(Disclaimer: Excel file attached below the post)

In case it isn't painfully obvious by now, I am fascinated by M&A and LBO transactions, and always have an eye out for a transaction that I might find intriguing; one such transaction was announced roughly two weeks ago when Model N (NYSE: MODN), a leader in revenue optimization and compliance for pharmaceutical, med-tech, and high-tech innovators, announced that it has entered into a definitive agreement to be acquired by Vista Equity Partners, a leading global investment firm focused primarily on enterprise software, data, and technology enabled businesses, for $30.00 per share (~$1.25B transactional value) in an all cash deal. I wanted to analyze the deal and see what the future holds for Model N, what changes, if any, Vista can make to boost the value of the company, and finally what the returns might look like at exit. I will succinctly talk about Model N, its strategy and future, and then delve right into the transaction.

Model N

Business

Model N is an industry leading provider of revenue management services within the life sciences and high tech companies; company's products and services allow companies such as Johnson & Johnson, AstraZeneca, Stryker, Seagate Technology and Broadcom in driving mission critical processes such as pricing, quoting, contracting, rebates and incentives. Model N's deep industry experience and its leading cloud-based technology have led to the firm's monumental success over the years. Historically speaking, companies, in this space, have relied on siloed and disjointed operations through manual processes, spreadsheets, and legacy systems to manage their revenue processes. Due to the isolation, these legacy operations often led to missed revenue opportunities, were labor intensive so led to higher costs, as well as being error prone and inflexible, rendering them ineffective in the current environment and most definitely obsolete for the future.

Model N expertise and cloud-based revenue management solutions, couple with the company's long operational history within this space, has enabled the company to develop software that is uniquely designed and architected to meet the business and strategic needs of these industries; such as managed care and government pricing for life sciences companies and channel incentives management for high tech companies; Model N Revenue Cloud transforms the revenue lifecycle into a strategic, end-to-end process aligned across the enterprise.

Products

Model N serves as one of the leading revenue management platforms for life sciences and high-tech industries. I think in order to understand what its future prospects look like, we need to first understand its offerings and services that have led to its enviable success.

Revenue Cloud for Life Sciences

Model N's suite of services and applications within the life sciences industry provide companies with end-to-end control and visibility across the company as well as assisting companies with corporate tasks such as customer relations management (CRM) and enterprise resource planning (ERP). The company provides following services within the life-sciences industry.

- Global Pricing Management: This service minimizes price erosion of products in international markets due to competitive pressures and/or government mandate through the product's lifecycle. Global Pricing Management allows companies to use Model N's services and platform to stay abreast of all the related current information that enables them to reach their metrics and margins.

- Global Tender Management: This service optimizes the bidding process and organizes the post-award tracking to efficiently manage the tendering lifecycle through automation.

- Provider Management: Manufacturers can utilize this product to manage complex institutional contracts with Providers. This particular service allows manufacturers to set up contracts using structured and organized pricing and price alerts for each product, allows price look up, and resolution and monitoring of end-to-end workflows.

- Payer Management: Minimized revenue leakage and noncompliance of complicated contracts with Payers. Payer management is an end-to-end industry leading management solution that helps eliminate revenue leakage in payer rebating processes.

- Government Pricing: Supports Federal government mandated calculations and reporting requirements for average and minimum prices achieved by manufacturers across their portfolio of products.

- Medicaid: Improves compliance and regulatory requirements and ensures payment of rebate claims on a timely basis and at correct rates for government Medicaid programs.

- Validata: Enables manufacturers to validate, summarize and analyze prescription level information in connection with processing of various forms of rebates to ensure accurate payments are made and duplicated reimbursements are avoided.

- Intelligence Cloud: Integrated business intelligence application to provide KPIs and trend analytics on all aspect of pricing, contracting, and discounting data across a host of solutions through easy configuration and centralized dashboard.

- Advanced Membership Management: Helps manufacturers manage their customers' membership with specific Group Purchasing Organizations (GPOs). This service also enables manufacturers in avoiding revenue leakage through validation eligibility for contracted pricing and ensuring compliance with specific rebate policies.

Revenue Cloud for High Tech

Model N's platform and services allow companies in the high-tech industry to adopt a strategic approach that enables the modernization of sales processes and therefore effective revenue management. Company provides following services to companies in high-tech industry.

- Deal Management: Enables companies with high deal conversion and pricing consistency with pricing, quotes, and contracts natively supporting the high-tech space.

- data Intelligence: Accords companies the ability to analyze historical deal data, and measure the impact of different pricing strategies and the impact on current deals.

- Channel Management: Provides manufacturers a more transparent view of their inventory as well as the ability to perform actions such as price protection, stock rotation and matching available inventory quotes.

- Market Development Fund Management: Allows companies to streamline their marketing development funds programs and reduce revenue leakage by increasing partner participation through a self-service portal.

- Rebates Management: Centralizes control of rebate programs to reduce upfront discounts and enables effective management of all incentives.

- Payment Management: Allows companies to pay, audit, and manage incentive payments globally while reducing costs to ensure accuracy and minimize revenue and opportunity leakage.

- NGage: An in-app guidance application that helps customers drive and measure channel/user adoption, change management and process excellence.

With an understanding of Model N's background, the industry it performs in, its offerings and services, the next thing that I would like to discuss are the company's strengths and its unique position in the industry that allows it to perform all of the above stated services with the utmost efficiency.

Strengths

- Comprehensive approach to revenue management: Model N's enterprise solutions provide a comprehensive look at the processes and provides end-to-end revenue management throughout the lifecycle of all products. This comprehensive approach makes it easy for Model N's customers to reverse the damage caused by siloed and disjointed operations and processes.

- Deep domain knowledge: Model N is considered an expert in the life sciences and high tech industries and, therefore, is uniquely positioned to provide solutions and services that are specifically catered for companies within this space.

- Strong customer base: The company, over the years, has established a reputation for delivering revenue management solutions to leading companies and have thus fostered long lasting and pivotal relationships; these relationships and the resulting recurring revenue allows the company to meet its internally set metrics and goals.

- Flexible deployment model: Model N possesses the ability to disperse its services and applications in multiple forms which gives the company a competitive advantage as well as the flexibility that is required by its customers; this flexibility enables Model N to deploy its solutions as SaaS applications, as fully managed and outsourced business services, or in a hybrid model mixing both SaaS and business services.

- Talented team focused on customer success: Model N employs experts and professionals that have been in the industry for a while now, and as a result, conduct a pivotal role in the company's success from developing services and applications to establishing business relationships as well as purveying its solutions to companies across the life sciences and high tech industries.

LBO Transaction

Setting the Stage

I think that I am in a comfortable position where I can safely analyze the company's future, the transaction and the returns. To start us off with the analysis, here are some preliminary assumptions and back of the envelop numbers that I think are tantamount to understanding this post.

As I mentioned at the start of the post, Vista offered $30 per share for all of Model N's outstanding shares, and given Model N's diluted shares outstanding of 40.8M, we get an offer value (equity value) of $1.225B, which, given Model N's last reported net debt of -$21M, yields an enterprise value of $1.204B. Additionally, Model N reported on its latest 8K an adjusted EBITDA of $42.9M, giving me an EBITDA multiple of 28.1x. The offered premium shown in my analysis is slightly different than the reported premium of 23% and that is because I am only comparing to the price from a month ago whereas the reported premium was based on the weighted average of Model N's share price for the last month. Some other assumptions that I made were about the minimum cash and the sources and uses of the proposed transaction; I am assuming that Vista will keep around $100M cash balance at minimum to support the working capital and other investment needs of the company going forward; I am assuming that the acquirer will opt to utilize the remaining cash balance of $201M to support the transaction as well as paying $1.3B of their own money. Since this a cash transaction, I am assuming that they will not use debt for this transaction, but I have left the functionality in the model because I will, towards the end, compare returns without debt to a scenario where they do take on debt. Let's now look at the historical income statement and understand the breakdown of its revenues and costs as well as its operating expenses and EBITDA.

Going back three years, Model N reported total revenues of $193M (FY '21), $219M (FY '22), and $249M (FY '23); company reported a revenue growth of 13% and 13.8% for the last two reported years. As is evident from the image above, subscription revenue constitutes for most of the company's total revenues with the company having reported subscription revenues as a percentage of total revenues of 74%, 73%, and 73% for FY '21, '22, and '23, respectively; professional services revenues constituted the rest of the revenues for the last three years, professional services revenues have been around the 27% mark of total revenues for the observed period. Furthermore, Model N has reported total costs of revenues of $97M (44% of total revenue) and $108M (43% of total revenue) for FY '22 and '23, respectively; company also reported operating expenses of $135M (61.6% of total revenue) and $145M (58% of total revenue) for FY '22 and '23, respectively. Company has additionally reported gross margins of 55% (FY '21), 55.7% (FY '22) and 56.6% (FY '23) as well as reporting net profit margins of -15.4% (FY '21), -13% (FY '22) and -13.6% (FY '23). Lastly, having rummaged through its 8K, the company reported adjusted EBITDA of $32M (14.6% margins) and $49M (17.2% margins) for FY '22 and '23, respectively. I will not being going over the company's balance sheet as I don't believe that it is relevant to our discussion or even accretive to the analysis. Let's now look at my assumptions about the company's future and see how they might impact the numbers for the next five years.

Assumptions (Base Case)

- Revenue Growth: I expect revenues to increase at a modest rate for the next five years. I believe that going forward subscription revenues will grow from 13.5% in FY '23 to 20% by the end of FY '28; I also believe that professional services revenues will grow from 14.7% in FY '23 to 18% in FY '28; I expect total revenues to grow from $249M (14% YOY growth) in FY '23 to $553M (19.5% YOY growth) by the end of FY '28. There are multiple factors that I believe will lead to this growth in revenues: I expect Model N's brand name, coupled with Vista's experience within the tech and enterprise software space, to play a pivotal role going forward; I also believe that Model N's deep knowledge of the industry will help the company in keeping its competitive advantage and keep improving its margins; I expect that Model N's customer base will not only persist, but will grow as the company spends more on R&D and sales and marketing for the next five years; some additional reasons for my expected revenue growth are its people, flexible method of deployment, increased enhancement of its services and platforms, and its comprehensive approach for revenue management.

- Costs of Revenue: This will be one of the many factors that the PE firm will be focused on in terms of improving margins along with inflating EBITDA and expanding the multiple. As Vista tries to grow the company in the coming five years, I expect that the firm will be able to reduce its costs concurrently with its revenue growth. I believe that, given their domain knowledge and experience with operating companies within this space, Vista will be able to reduce costs of subscription revenues from 35% as a percentage of subscription revenues to 30% by the end of the holding period as well as reducing costs of professional services revenues as a percentage of professional services revenues from 66% in FY '23 to 55% by the end of FY '28.

- Operating Expenses: Model N's operating expenses consist of research and development costs, sales and marketing, and general and administrative; as the company grows and gets more efficient in terms of generating more revenues from its current clients as well as onboarding more clients and developing professional relationships at a minimal cost, its operating expenses should reduce throughout the holding period as a percentage of total revenue. I expect the company to keep investing in its R&D in order to sustain and support the growth in revenue, furthermore, I believe that as the company tries to grow its revenues, it will need to invest in R&D to enhance its current offerings and services as well as developing and using new technologies to entice more and more companies to use its platform. As the company grows and gains a firmer foothold within the industry, I believe that sales and marketing costs should reduce as a percentage of revenue; I expect sales and marketing to reduce from 21.7% in FY '23 to 20% by the end of the FY '28. Lastly, I believe that Vista, in conjunction with Model N's management, will be able to reduce its headcount and other administrative charges from 17.2% to 15% as a percentage of total revenue. Overall, I expect total expenses as a percentage of total revenues to go downhill from being 58.3% in FY '23 to 54% by FY '28.

- Asset Utilization: Better asset utilization is one of the levers of a private equity transaction, and given that we are analyzing this transaction, I am assuming that Vista has recognized better ways to utilize Model N's assets in order to reduce the associated costs and increase the incremental revenues.

- Multiple Expansion: Multiple expansion is by far one the difficult paths to inflate returns for an investment firm; it is a gargantuan task because not only does it depend on how the company performs, but also on the macro trends. Multiple expansion relies on tentative issues such as the market conditions, interest rates, future valuations, buyers' sentiments, and the industry outlook, issues that no one can honestly predict. With that being said, there are less than ideal ways to inflate multiples by the time of the exit and they include but are not limited to geographic expansion, more long-term contracts with companies, product diversifications, and a better outlook for the company and the industry. Additionally, given that Vista dabbles in technology and enterprise software companies, they might be able to bolt-on another company onto Model N down the road in order to attain steroidal returns.

- EBITDA Expansion: Unlike multiple expansion, EBITDA expansion is an attainable goal, and given my assumptions surrounding revenue growth and reduction in costs, I expect Model N's adjusted EBITDA to grow from $42.8M (EBITDA margins of 17.2%) in FY '23 to $111.03M (EBITDA margins of 20%) by the end of FY '28.

- Deleveraging: I have not assumed any debt for this transaction, but I will play out a scenario by the end of the post where I do look at the possibility of assuming debt for this purchase and how Model N and Vista could go about paying it off early in order to get the desired fortuitous returns; as the model will show, the company barely generates enough cash flows to support interest payments let alone the associated mandatory amortization and any discretionary payments for term loans.

- Vista's Portfolio: Vista's is an investment firm that is known worldwide for its expertise in enterprise software, data, and technology businesses, and I believe that the firm will be able to, if not exceed, my revenue estimates and cost reductions and should very easily be able to realize their expected returns. I further believe- given my projections- that Vista will more than likely add another company onto Model N in order to not only inflate revenues but also to increase their returns through synergies, pricing power, bargaining power, lower CAC, and an improved cost structure.

With all of our assumptions out of the way, here is a look at the forward looking income statement and gross, net profit and EBITDA margins.

As you can see, I expect Model N's total revenues to increase from $249M in FY '23 to $553M by the end of FY '28; I expect total costs of revenues to reduce from being 43% of total revenues in FY '23 to 36.7% by the end of the holding period. As is also evident from the screenshot above, I expect total operating expenses to reduce from being 58% of total revenue to around 54% by the end of FY'28. I expect the company to report a positive EBIT by the end of the first year and the reason is two-fold: first and foremost, I am assuming a growth in revenues and reduction in costs so more funds are flowing towards the operating income, and secondly, I am assuming an all cash payment and no debt involved which means that there is no interest expense. In terms of margins, I expect the company's gross margins to improve from 56.6% in FY '23 to 63.3% by FY '28; furthermore, as stated in the assumptions, I expect EBITDA margins to improve from 17.5% in FY '23 to 20% by FY '28. Here is what I think the balance sheet line items could like in the future:

As you can see, Model N (in my base case) is generating a healthy amount of free cash flows with projections increasing from $44M in FY '24 to $103M by the end of FY '28; as stated before, please bear in mind that these excess cash flows are majorly due to the fact that we are not assuming any debt in this transaction, this of course also makes it relatively easier for Vista to pay itself a dividend down the lane to spice up their returns even more. Now, for the sake of this particular conversation, if I assume that Vista ends up raising ~$1.4B in debt, here is how drastically different the cash flow statement might look like:

As you can clearly see, the company does not have enough cash remaining after making the interest payments and the mandatory amortization, as a matter of fact, the model predicts that they might need to draw down on their revolver to break even. There are of course a thousand different ways this could go, but I just wanted to highlight the company's ability, or lack thereof, to meet its debt obligations. With income statement, balance sheet and cash flow statement explained, let's now move on to the crux of the analysis: the returns.

Returns:

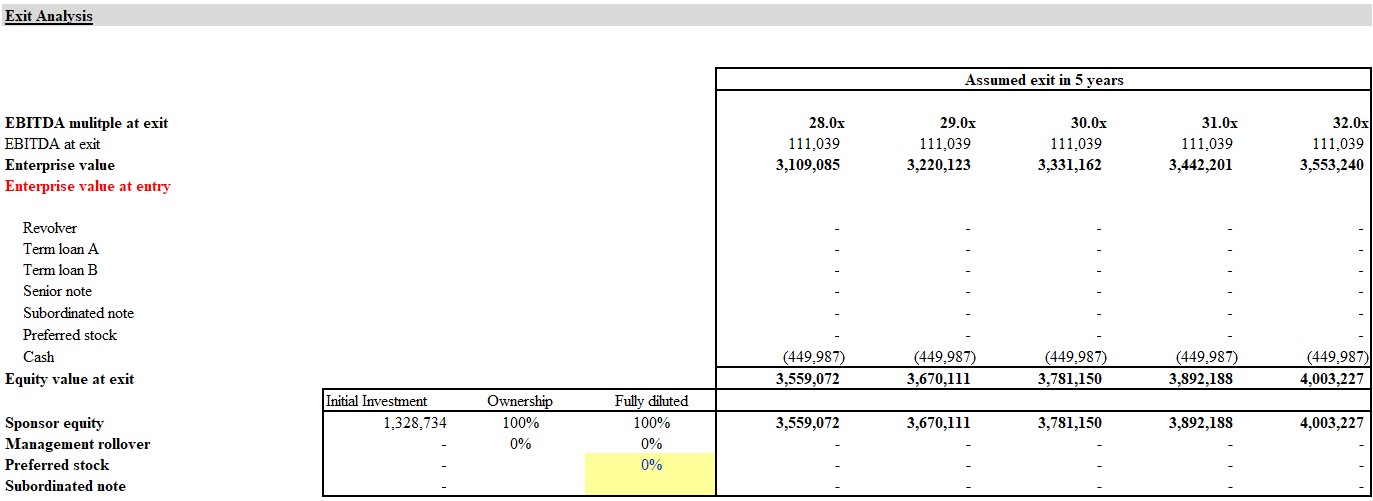

I think that I am in a decent place to now discuss the possible returns for Vista, I think it is important to notate here again that these returns are based on the fact that there is no debt raised and that Vista is paying for the entire transaction with their available powder, with that side note, lets look at the possible enterprise and equity values at different multiples.

As you can see, assuming the same exit multiple and no other dilution from preferred, management or subordinated equity providers, we get an enterprise value of $3.1B, and given the accumulated balance of cash of $449M, we get an equity value of $3.56B. Of course, if Vista is somehow able to expand their multiple and get a higher multiple at the time of exit, say 30x, the enterprise value would be $3.3B, that would give us an equity value of $3.78B. Let's now look at IRR and MOIC at different multiples.

Assuming that Vista pays around $1.5B (including fees and Model N's cash balance) and exits at the same multiple that it entered at- 28x- the firm could expect (in my base case) a money on invest capital (MOIC) of 2.7x and an internal rate of return (IRR) of 22%; you might be tempted to ask, "Is that good? Bad? In line with their expectations?" Those are all questions that people that worked on the transaction could answer in a far more intricate manner than I can- all I can say is that given the environment we are in, those returns don't seem too bad to me. Again, this was assuming that Vista pays in cash and raises no debt so the returns could be low due to multiple reasons: firstly, Vista is putting in a lot at the beginning which is why their returns are in low twenties; secondly, I am assuming the same exit multiple, but the returns could be higher if they are able to expand the multiple; and lastly, they might be able to grow the revenues, reduce costs, and expand EBITDA in a far more fashioned and nuanced way than I am anticipating. The lower section of the screenshot highlights the maximum amount Vista can offer given their various internal rates of return. For instance, if we assume that the company will exit at 28x and the equity value of $3.56B, then assuming that their minimum hurdle rate is 25%, they can only afford to offer $1.06B as opposed to $1.23B.

One last thing that I would like to look at are the returns if they do decide to take on debt; lets assume that Vista chooses to only use $505M of its own cash balance and raises around $857M in debt, here is how the returns might change.

As you can see, if Vista puts in less of its own money and raises debt, then assuming the same multiple of 28x, we get a MOIC of 5.2x and an IRR of 39%, considerably higher than the returns if no debt was raised. Again, assuming debt, given a minimum hurdle rate of 25%, Vista can afford to offer $1.56 as opposed to $1.23B.

Conclusion

This is of course an academic exercise aimed primarily at quenching my own curiosity than validating or reaffirming the transaction, with that being said, I think this could prove to be a lucrative deal- how lucrative? Only time will tell. I think I have gone on for far too long, and so I will end it on the note that the value of anything is in the eye's of the buyer.

Links:

I recommend that you download and open the below attached file in Excel rather than opening it online in Google Sheets.